The Of Mortgages

At that point, the earnings from the sale of the house (or another resource) can settle the reverse mortgage balance. The earnings received from a reverse home loan are complimentary from federal and state earnings tax and can be used for any purpose. The interest that eventually will be paid when the reverse home mortgage is retired is tax-deductible, however only at the point when the reverse home mortgage is paid off.

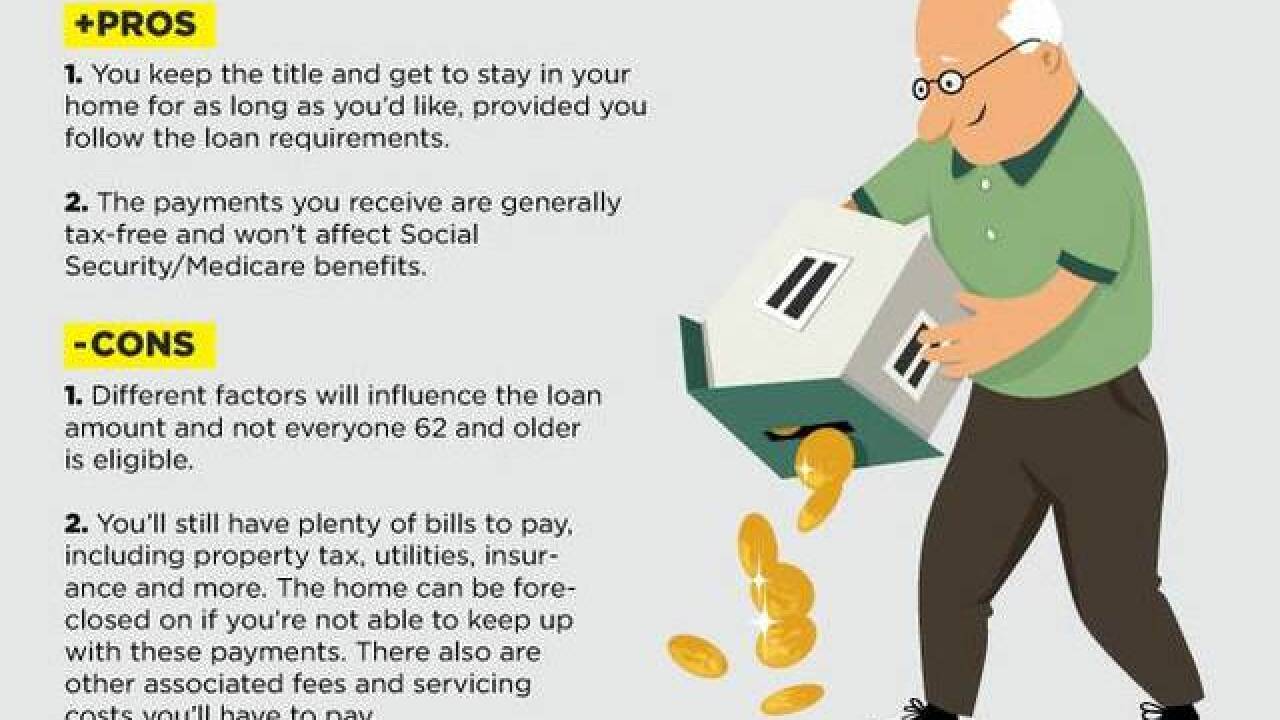

The age of the borrower and the worth of the customer's house are two main aspects affecting the quantity of a reverse home loan. The older the debtor, the more they can borrow. Likewise, the greater the worth of the home (approximately specific limitations), the more they can obtain. The typical quantity of a reverse mortgage is roughly 50 to 60 percent of a home's value.

A 3rd factor affecting reverse mortgages is the dominating rates of interest. If you prepare to live in your house up until you pass away, a reverse home loan might use you a considerable source of cash. Perfect candidates for a reverse mortgage will remain in excellent health, in their later 60s or older, and have long life spans of 15 or more years.

The 45-Second Trick For Mortgages

Since of the high upfront expenses of reverse mortgages, they need to be assessed carefully. In the past, reverse home mortgages were thought about a last option to utilize after all other financial resources (individual savings, retirement accounts, the cash value of insurance coverage, etc.) were exhausted. There is a school of thought, however, that reverse home mortgages may serve other functions and financial objectives, such as providing an income source to postpone making an application for Social Security advantages or to pay taxes due on Roth IRA conversions.

The greatest advantage to a reverse home loan is that it enables you to obtain versus your own equity while retaining ownership of your home. It's a terrific option for seniors who need a little additional month-to-month income to cover medical expenses or other unanticipated financial responsibilities. In fact, there are no limitations on how you can use funds from a reverse home loan.

For instance, loan origination fees, appraisal expenses, and interest can quickly amount to countless dollars, so this requires to be a figuring out factor when deciding whether a reverse home mortgage is your best alternative. Furthermore, considering that you'll need to repay your reverse home mortgage when you vacate the home, offer it, or die, a reverse home https://en.search.wordpress.com/?src=organic&q=reverse mortgages mortgage may prevent you from keeping your house "in the household," which is a deal-breaker for some.

Unknown Facts About Reverse Mortgage Reverse Mortage Tips

Need a little additional cash as you head into retirement? Heard of reverse mortgages however do not understand how they work? Canstar explains what a reverse mortgage is and what to be familiar with before signing on the dotted line There are numerous methods to spend for costs that come up in retirement; sign up with a Kiwi Saver scheme to develop a retirement cost savings pot, guarantee your house is settled and use your own cost savings to supplement the Government's Superannuation scheme.

But entering a reverse mortgage contract is not a choice to make lightly. Canstar takes a look at what you must think about before securing a reverse home mortgage in New Zealand. A reverse home loan is targeted at individuals aged 60 or over who have substantial equity in their home. According to the New Zealand Federal government site, you can get a reverse mortgage if you've settled your mortgage, or only owe a little quantity.

The loan provider is likely to have a minimum age requirement to use-- frequently 60 years of age. Reverse home mortgages suggest the debtor can access the equity, without having to pay back the service or loan while they still reside in the house. The cash from reverse mortgages may be invested in day-to-day living costs and purchases, such as likewise use reverse home loans to pay off other financial obligations, such as house enhancements, according to a leading reverse home loan loan provider, Heartland Bank.

The Mortgages PDFs

On the other hand, you still own https://www.washingtonpost.com/newssearch/?query=reverse mortgages your house and continue to earn any capital gain as it grows in worth. A reverse mortgage brings with it risks that the worth of the property involved does not grow as rapidly as anticipated, or perhaps that the home value might drop, the Reserve Bank of New Zealand (RBNZ) states.

The power of substance interest might likewise turn the loan into an unfavorable equity. RBNZ, therefore, figures out that reverse home mortgages have a higher threat profile than that of standard mortgage. Compare present mortgage rates with Canstar In 2015, regardless of pushback from banks, RBNZ cracked down on policies around reverse equity mortgages, out of concern that lending institutions would be left in strife if house costs drop or rates of interest rise.

Reverse equity home mortgages all however Helpful site dried up after the worldwide monetary crisis in 2007 to 2008, with lenders http://www.bbc.co.uk/search?q=reverse mortgages closing their books on brand-new organisation for this type of financing. However, reverse home loans remain a key part of Heartland Bank's loaning, according to the bank's site. Registering with a reverse mortgage lending institution is not something to rush into.

The Ultimate Guide To Mortgages

Get financial and legal suggestions before signing up. We likewise recommend consulting with your household. Even though you do not require to make repayments, as discussed earlier you require to focus on compound interest, as it can rapidly increase the financial obligation. This problem is more heightened if property costs do fall.

It's essential to note that rates of interest on reverse equity home loans are generally greater than rates for regular house loans. One of the concerns to ask is whether the provider is ethical. You must likewise ensure that the loan provider can use the following assurances: you won't be dislodged of your house for as long as you select to reside in it.

As the current generation retires, ideally there will be no requirement for reverse equity home loans. If everybody contributes to Kiwi Saver now, they'll have a good quality financial investment portfolio on retirement and will not require to obtain versus their homes. Reverse home loans are targeted at those of retirement age and who have considerable equity in their home.

Getting My Reverse Mortgage To Work

These loans have a higher threat profile than basic house loans therefore have greater risk weightings. It's essential to guarantee reverse home mortgage loan lenders are ethical, for instance, check that you won't be displaced of your house for as long as you pick to live in it. Compare House Loans with Canstar.

The Chief law officer provides Customer Alerts to inform the general public of unjust, misleading, or misleading company practices, and to offer info and assistance on other issues of issue. Consumer Alerts are illegal guidance, legal authority, or a binding legal opinion from the Department of Attorney General Of The United States. Reverse home loans have actually become an increasingly popular option for seniors who require to supplement their retirement income, pay for unforeseen medical expenses, or make required repairs to their homes.