The Main Principles Of Residential Mortages

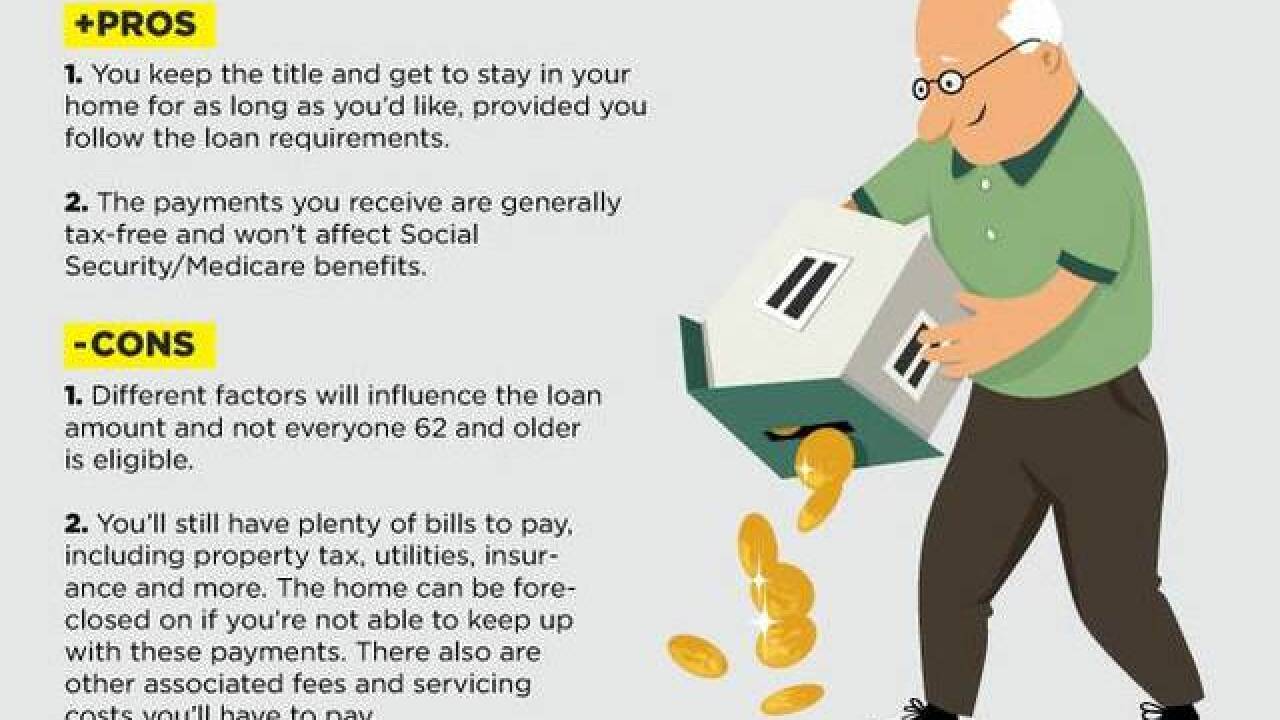

Although you are not accountable for making month-to-month payments on the loan, due to the fact that you stay the owner of the house, you continue to be accountable for paying home taxes, keeping homeowners insurance coverage, and making necessary repair work. The HECM is the most popular reverse home loan. HECMs are guaranteed by the Federal Real Estate Administration (FHA), which is part U.S

. The FHA warranties that lenders will meet their obligations. HECMs are just used by federally-approved lenders, who are required to follow rigorous rules imposed by the federal government. The FHA informs HECM lenders how much they can provide you, based on your age and your home's value. Further, you need http://www.bbc.co.uk/search?q=reverse mortages to go through reverse home loan counseling as a condition to obtaining this kind of loan.

These kinds of reverse home loans are offered by state and regional federal governments, or not-for-profit lenders, and are generally the least costly reverse mortgages. They are typically only readily available to low to moderate income property owners. Some banks and monetary institutions provide their own reverse mortgages. These loans are backed by the personal companies that offer them; they are NOT insured by the federal government.

Unknown Facts About Residential Mortages

The house protecting the reverse mortgage must be your primary house. Eligible home types include single-family houses, 2-4 unit owner-occupied residential or commercial properties, produced houses, condominiums, and townhouses. You should either settle the old home loan financial obligation before you get a reverse home mortgage, or settle the old mortgage financial obligation with the money you receive from a reverse home mortgage.

Similar to all home loans, there are expenses and costs connected to securing a reverse home loan. Charges include those related to loan origination, home mortgage insurance premiums, closing expenses, and monthly servicing fees. These costs are typically greater than the costs associated with conventional home mortgages and house equity loans. Make sure you understand all the expenses and charges connected with the reverse home loan.

You usually do not have to repay the reverse home loan as long as you and any other borrowers continue to live in the home, pay residential or commercial property taxes, maintain property owners insurance coverage, and keep the property in great repair. Your reverse home mortgage lending institution may include other conditions that will make your reverse home mortgage payable, so you ought to home movies mortgages and marbles read the loan files thoroughly to make sure you comprehend all the conditions that can trigger your loan to end up being due.

Not known Incorrect Statements About https://hattielenoredeweyydcb.page.tl/How-To-Explain-Reverse-Mortage-Tips-To-Your-Mom.htm Residential Mortages

If this amount is less than your home deserves when you repay the loan, then you (or your estate) keep whatever amount is left over. With a lot of reverse home mortgages, you can never ever owe more than your house deserves. The technical term for this cap on your debt is a "non-recourse limit." It suggests that the lender, when looking for payment of your loan, typically does not have legal option to anything other than your house's value and can not look for repayment from your heirs.

Speak with an independent financial consultant to discover what reverse home mortgage bundle finest suits your monetary circumstance Mortgages and requirements. If you do not have a monetary advisor, discuss your circumstance with a therapist authorized by the US Department of Real Estate & Urban Development (HUD); HUD-approved counseling agencies are offered to help you with your reverse home loan questions.

Make sure you understand all the expenses and charges connected with the reverse home mortgage. Discover whether the reverse home mortgage you are considering is federally-insured. This will secure you when the loan comes due. Discover out whether your repayment commitment is restricted to the worth of your home at the time the loan becomes due.

The Best Guide To Reverse Mortgage

Watch out for anybody who tries to pressure you into a decision that you are not entirely comfortable with, such as investing the payments from your reverse home mortgage into an annuity, insurance plan, or other financial investment product, or pressing you into receiving a lump-sum payment over monthly payments. If you are uncomfortable with the reverse mortgage that you participated in, exercise your right of rescission within 3 days of the closing.

concerns of interest to senior citizens. Customers may contact the Lawyer General's Customer Security Department at: Consumer Protection Department P.O. Box 30213Lansing, MI 48909517-335-7599Fax: 517-241-3771Toll complimentary: 877-765-8388Online grievance type.

The boosted equity in the house can be utilized to get a loan through a 'reverse home loan,' offered just to senior citizens. Typically individuals use the earnings from a reverse mortgage in a type of financial investment that offers income payments at routine periods called an 'annuity,' or they established an open line of credit, or take monthly payments.

Reverse Mortgage - An Overview

Reverse mortgage arrangements supply that no payments are due till the house owner passes away, or the house is offered or deserted. Unless you fall behind on taxes or allow your house to slip into disrepair, the lending institution can't foreclose on the property. You can continue residing in your house even if you live lots of years beyond http://edition.cnn.com/search/?text=reverse mortages expectations and the size of the financial obligation surpasses the worth of the home itself.

Lenders also take into account your age, the appraised value of your home, existing rates of interest and where you live. Usually, the older you are, the bigger Reverse Mortgage the loan you will be able to get. The Financial Consumer Agency of Canada sets out some of the benefits and downsides of a reverse home loan: You do not need to make any regular payments on the loan.

The money you borrow is a tax-free income. This earnings does not impact the Old-Age Security (OAS) or Ensured Earnings Supplement (GIS) advantages you might be getting. You maintain ownership of your home. You can choose how you want to get the cash. You can select to get: a lump-sum payment a loan to set up planned advances that offer you with a routine income, or a combination of these choices.

The Buzz on Residential Mortages

The equity you hold in your house will decrease as https://www.washingtonpost.com/newssearch/?query=reverse mortages the interest on your reverse home mortgage compounds and builds up over the years. If you are forced to sell your house due to the fact that of a change in circumstances, there can be a lot less of the earnings readily available for alternate housing, etc

. The time needed to settle an estate can frequently surpass the time permitted to pay back a reverse mortgage. For complete information, check with the reverse home loan loan provider. Given that the principal and interest will be paid back to the lending institution at your death, there will be less cash in your estate to leave to your kids or other successors.

They can include: a home appraisal cost, application fee or closing fee, costs for independent legal recommendations, a higher interest rate than for a conventional home mortgage or line of credit, a repayment penalty for selling your house or moving out within 3 years of acquiring a reverse home loan. CHIP is the source of many reverse home mortgage items that are available in Canada.

More About Reverse Mortgage

It is not connected with CMHC. With a CHIP House Income Plan, you get a loan for as much as 40% of the value. The interest is currently at a rate 1 1/2% above a routine 5 yr mortgage rate. Again you do not need to make any payments-- interest or principal-- for as long as you or your spouse reside in your house.